Bad News and Good About the LNG Crisis

The war shut down every long-term supplier in a week. But the permanent damage may not be Bangladesh’s problem.

There has been a lot of confusion around the LNG situation -- what Qatar’s force majeure declarations mean for Bangladesh, whether we’re locked out of supply for years, and how bad this really gets. I’ve spent some time digging through the contracts, the train structures, and the actual supply chain to try and make sense of it.

What follows is my attempt at a clear-eyed breakdown. Data first, then analysis. The numbers are ballpark -- directionally accurate, not audited to the decimal.

The Contract Landscape

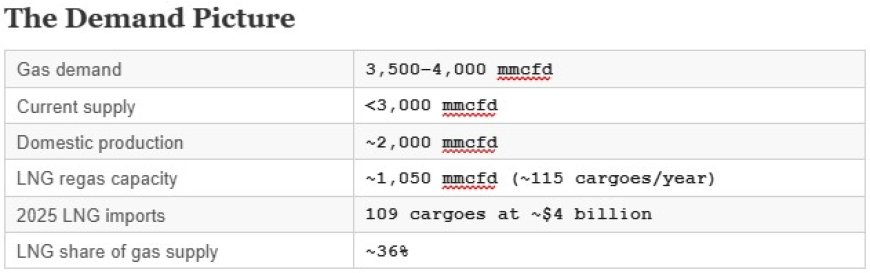

Bangladesh purchases LNG under two types of arrangements. Long-term contracts are priced on a formula tied to Brent crude oil -- something like 13% of Brent + $0.40 per MMBtu. These give you cost predictability. And then there’s the spot market, where prices are set by real-time global supply and demand through a bidding process. Spot LNG currently costs almost double the long-term contract rate.

First, let’s look at the long-term deals Bangladesh has in place.

A note on Excelerate. They are essentially a middleman. They procure the same LNG from QatarEnergy -- buy it FOB at Ras Laffan, arrange the shipping, and regasify it in Bangladesh using their own FSRUs. It’s a convenience arrangement. Under the other long-term contracts, Petrobangla has to schedule shipping, coordinate FSRU logistics, and manage the supply chain itself.

And then there’s the spot market -- where governments scramble to buy whatever LNG isn’t tied up in long-term contracts globally. Bangladesh was supposed to buy about 30 cargoes from the spot market in 2026.

In total: ~86 long-term cargoes + ~29 spot cargoes = ~115 planned cargoes for 2026.

The Analysis

The plan was quite rational. Long-term contracts are cheaper than spot. Bangladesh was locking in as many long-term deals as possible through 2023, which would have dropped the spot market ratio from roughly 50% to just 25% of total imports. More predictability, lower costs, better energy security.

Then the war came. And within the space of five days, the entire strategy unravelled.

On March 2, QatarEnergy halted all LNG production across all 14 trains at Ras Laffan. By March 4, they had formally notified buyers -- including Petrobangla -- of Force Majeure. OQ Trading followed on March 5. Excelerate on March 6. Every single long-term supplier went dark simultaneously.

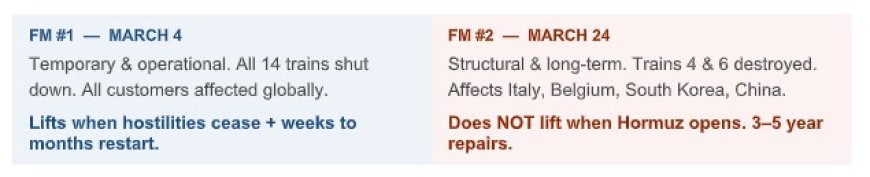

This was Force Majeure #1 -- a temporary, operational shutdown triggered by the closure of the Strait of Hormuz and the broader security situation. It wasn’t about damaged infrastructure. It was about the fact that tankers couldn’t leave and the region was under fire. This FM affects every QatarEnergy customer globally -- not just Bangladesh.

Then, on March 18–19, Iranian missile strikes physically destroyed two of Qatar’s 14 LNG trains. On March 24, QatarEnergy declared Force Majeure #2: A separate, structural declaration covering only the long-term contracts tied to those two damaged trains. The affected customers are China, South Korea, Italy, and Belgium. This FM won’t lift when Hormuz reopens. Those trains are physically wrecked. Repairs will take 3 to 5 years.

These are two completely different events. Bangladesh is caught in FM #1 -- which is painful but temporary. Bangladesh is most likely not a party to FM #2 -- which is the truly devastating, years-long one.

But let me explain why.

If the Strait of Hormuz Stays Closed

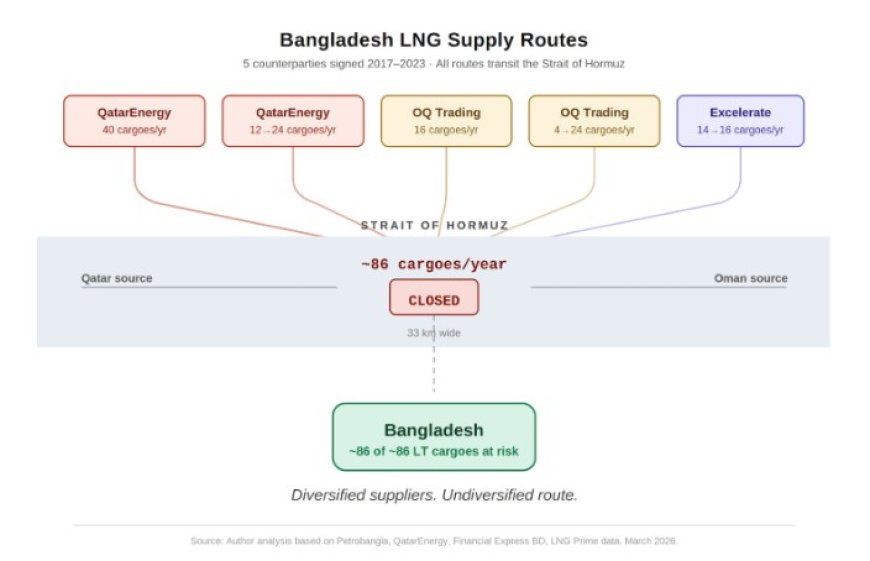

Qatar and Oman are both exposed to the Strait of Hormuz. As is Excelerate, since it sources from Qatar. If Hormuz doesn’t reopen, Bangladesh’s entire long-term contract portfolio -- all ~86 cargoes -- is out of commission. Every single one has to transit through a strait that is currently closed.

The entire LNG need would have to be met from the spot market. Realistically, Bangladesh won’t be able to procure the volume it needs while competing against Japan, Korea, China, India, and the EU for a thin pool of available cargoes. There simply isn’t enough uncontracted supply globally. And just money won’t buy it.

If supply is available, Bangladesh might secure between 40% and 70% of its annual need. It will pay more and buy less. The reserves are there -- over $34 billion gross, roughly $29 billion readily usable under IMF methodology. Bangladesh will probably end up spending about the same amount it spent in 2025 and getting about half the gas from LNG.

The crisis will be more on the gas supply side than on the reserve or currency side.

If the Strait of Hormuz Reopens

This is where the two force majeures need to be understood separately.

The Devil’s in the Contracts

The Devil’s in the Contracts

QatarEnergy is actually a merger of two formerly separate companies -- Qatargas and RasGas. Bangladesh’s original deal (QatarEnergy, 40 cargoes) was signed with RasGas.

LNG trains are usually structured as joint ventures with different equity partners. Legally, each train or group of trains operates as a separate commercial entity -- with its own customer base, accounts, and cash flows. It is not like all LNG goes into a single pot and gets shipped out proportionally. Even though QatarEnergy runs the complex as one integrated operation, when it comes to selling the LNG, each JV has its own contracted buyers. If one JV can’t deliver due to force majeure, they can’t simply redirect LNG from another JV’s production -- those molecules are already spoken for under separate contracts.

The damaged trains -- Train 4 and Train 6 -- serve China, South Korea, Italy, and Belgium. Bangladesh’s legacy contract is connected to different, intact RasGas-era trains. QatarEnergy typically owns roughly two-thirds equity in each train, with the remaining third held by various international energy companies -- ExxonMobil, Shell, ConocoPhillips, KOGAS, Mitsui, and others, depending on the specific JV.

Bangladesh has diversified its suppliers. But it has not diversified where the LNG comes from. It diversified the counterparty names, not the geographical or geopolitical risk.

What happens to each of Bangladesh’s contracts if Hormuz reopens?

CONTRACT-BY-CONTRACT — IF HORMUZ REOPENS

QatarEnergy — 40 cargoes/year ✓ RESUMES

Connected to RasGas’s legacy trains, which are intact. Once Hormuz reopens, it will take several weeks to months to restart. After that, business as usual. No long-term impact as of now.

OQ Trading — 16 cargoes/year ✓ RESUMES

OQ Trading is an aggregator. Once Hormuz opens, they resume exporting.

QatarEnergy — 12→24 cargoes/year ⚠ DELAYED

This is the tricky one. This contract is tied to Qatar’s new North Field East expansion trains, which haven’t been built yet. The war has likely pushed their startup past 2026. Worth watching closely — this contract is crucial for medium-term energy security.

OQ Trading — 4→24 cargoes/year ✓ RESUMES

Should be fine once Hormuz opens. Small volume in 2026 regardless — only 4 cargoes planned for the first year.

Excelerate — 14→16 cargoes/year ○ DEPENDS

Depends on both Hormuz reopening and QatarEnergy restarting, since Qatar is the source. Excelerate does have some Louisiana-sourced volumes through a deal with Venture Global, but I’m fairly certain those aren’t earmarked for Bangladesh. Keep in mind: If a company can legally pause delivery on one contract and sell at double the price on the spot market, it will. Excelerate may have kept this option open.

Bottom Line

If the Strait of Hormuz reopens, Bangladesh can breathe. The damaged QatarEnergy infrastructure -- the two destroyed trains -- likely does not have a direct impact on Bangladesh’s contracted supply. The trains serving Bangladesh’s contracts appear to be intact.

The indirect impact, however, is real. The buyers who were earmarked for the damaged trains -- China, South Korea, Italy, Belgium -- will now compete aggressively in the spot market for replacement volumes. That drives up prices for everyone, including Bangladesh.

And on the diversification point: Bangladesh imported a grand total of one LNG cargo from Angola in its April schedule. One out of eleven cargoes from a non-Hormuz route. That’s the extent of the geographical diversification. I wonder whether the previous government’s troubled relationship with the US in 2023 played any role in the absence of direct US-sourced LNG contracts.

Going forward, finding the LNG to buy will be a bigger problem than reserve depletion. Large economies will deploy all their soft and hard power to procure gas. Japan, South Korea, and India all have better bargaining chips in this situation compared to Bangladesh. China and Pakistan have their own leverage to ensure they get priority access.

Two things to keep in mind. One issue is LNG production. The other is transportation. If Hormuz is closed, transportation is the bottleneck -- the problem isn’t making the gas, it’s moving it, and everyone is affected. If Hormuz reopens, then only the buyers of the physically damaged trains remain affected, because that production capacity is gone for years.

For Bangladesh, the first problem is the immediate crisis. The second -- mercifully -- appears to be someone else’s.

Disclaimer: All figures are approximate and based on publicly available reporting from Financial Express BD, The Business Standard BD, LNG Prime, Petrobangla data, QatarEnergy official statements, IEEFA, Al Jazeera, CNBC, Reuters, and other sources. Train-to-contract mapping is inferred from public statements — QatarEnergy does not publicly disclose internal production allocation. This is not investment or policy advice.

Taukir Aziz is a specialist in personal finance and currently serves as a tax and investment planning specialist at Credyt.

What's Your Reaction?