Emerging Markets Monitor

The Strait of Hormuz is in crisis, disrupting the global economy. Asia, in particular, faces a coming storm with a prolonged closure -- the Strait carries the lifeblood of Asia's economy.

When the story of the first quarter of the twenty-first century will be written, the rise of Asian economies -- notably China, India and southeast Asia as well as the acceleration of South Korea and Taiwan -- will play a leading role.

The emergence (or, rather, re-emergence) of Asian economies as major players on the world stage has not only shifted trade patterns, supply chains, and national wealth distribution, but has also re-shaped global geopolitics.

Asia’s rise, however, has had a key ingredient: Middle East energy. Oil and gas exports, mostly from the Persian Gulf region, have literally fueled what some are calling the Asian Century.

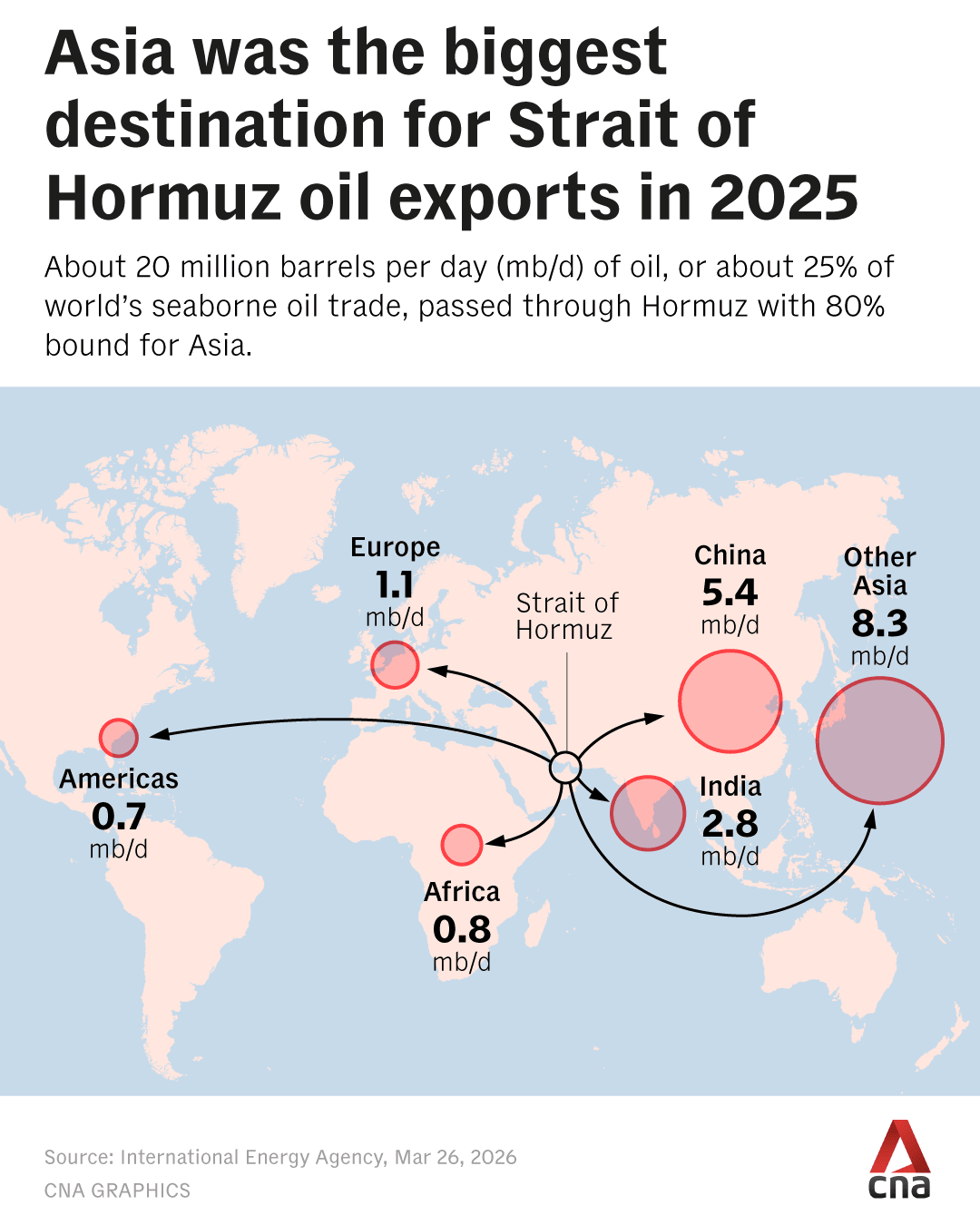

Consider this: Some four out of five barrels of oil that exit the Strait of Hormuz head to Asia. Roughly the same calculation for the liquid natural gas (LNG) that powers Asian economies. Last year, 82% of Qatar’s LNG went to Asia, according to Bloomberg data.

Then, there’s aluminum, fertilizers, liquefied petroleum gas (LPG), helium, petrochemicals, and jet fuel, all of which flow in significant volumes from the Persian Gulf to global markets, particularly Asia. Over the past several decades, Gulf Arab states have moved well beyond their role as raw commodity exporters, building sophisticated downstream industries that leverage abundant, low-cost oil and gas feedstock.

Today, they are not just energy suppliers but critical providers of industrial inputs that underpin manufacturing, agriculture, transportation, and technology supply chains across the global -- and especially Asian -- economy.

In terms of sheer trade volume, the Strait of Hormuz is not the world’s busiest chokepoint, nor Asia’s busiest. That distinction belongs to arteries like the Strait of Malacca and the Suez Canal, which carry larger volumes of global commerce.

But Hormuz is different. It is the world’s most concentrated conduit of energy and industrial inputs, much of which has few, if any, substitutes. And unlike Suez, where ships can reroute around the Cape of Good Hope at higher cost and delay, there is no meaningful immediate workaround to Hormuz.

That vulnerability helps explain why the Islamic Republic of Iran has targeted the Strait of Hormuz in response to US and Israeli strikes that began on February 28 and have severely degraded its navy, missile capabilities, and nuclear potential -- as well as killing several of its top political and military leaders. Iran cannot match the United States or Israel in a conventional war. Instead, it is reaching for its most powerful asymmetric lever: The Strait of Hormuz.

Tehran is applying pressure where it matters most, by threatening the flow of energy and industrial inputs through the Strait. As Sultan Al Jaber, the UAE Minister of Industry and Advanced Technology and Managing Director and Group CEO of ADNOC, put it in the Wall Street Journal, “By taking Hormuz hostage, Iran is committing global economic warfare.”

Iran has also targeted its Gulf Arab neighbors across the water -- with the UAE its most frequent target -- despite the fact that they all lobbied Washington to avoid war with the Islamic Republic and a détente had been growing between Tehran and erstwhile foes in Riyadh and Abu Dhabi.

Iran has hit energy and industrial infrastructure across multiple Gulf Arab states, including LNG, oil, and processing facilities, striking at the core of the region’s economic lifelines.

Beyond the pain felt in the Gulf Arab states by Iran’s strikes, the most concentrated pain will be felt in Asia and further afield, in many of the Global South countries that are less equipped than advanced economies to ride out an economic storm.

Many emerging economies -- from South Asia to Sub-Saharan Africa and parts of Latin America -- are heavily dependent on imported fuel and fertilizers, leaving them acutely vulnerable to price spikes. For these countries, higher energy costs are not just a macroeconomic headwind. They translate directly into rising food prices, worsening trade deficits, currency pressure, and heightened risks of social and political instability.

For Asian economies, however, the story runs even deeper. It’s no exaggeration to call the Strait of Hormuz a de facto “Strait of Asia” -- a critical energy lifeline that rivals the importance of the Strait of Malacca, which connects the Indian and Pacific Oceans.

Losing Sleep Over Hormuz

On one of my visits to Tokyo several years ago, a Japanese foreign ministry official told me: “We think a lot about the Strait of Hormuz and lose sleep over it because that’s part of our job, but for most Japanese, they hardly ever think about it all.” Japan -- one of the world’s top oil importers -- sources 95% of its imports from producers within the Gulf region. That’s enormous concentration risk, and certainly a good reason to keep all Foreign Ministry officials up at night.

He is no longer alone. Many are losing sleep over Hormuz now.

Over the past week, I scoured my library Bloomberg terminal, talked to specialists, read industry newsletters, and generally did a deep dive into what goes in and out of the Strait of Hormuz. I’m sharing with you some of the nuts and bolts below, and how they affect Asia, in particular.

Let’s start with oil.

Oil - Four out of Five Barrels

About 20% of the world’s petroleum liquids consumption passes through the Strait of Hormuz. More than four-fifths of the crude and condensate moving through the Strait heads to Asia, with China, India, Japan, and South Korea the top destination markets. The United States, by contrast, is only marginally exposed: in 2024 it imported about 0.5 million barrels a day through Hormuz, equal to roughly 7% of its crude and condensate imports and 2% of its petroleum liquids consumption.

The Asian economies most exposed to a Hormuz disruption are Japan and South Korea most acutely, with China and India also heavily vulnerable because of the sheer scale of their Gulf oil intake. The below are four of the biggest buyers of Middle East crude, with their percentage of imports that flows through the Strait of Hormuz.

- Japan - 95%

- South Korea - 71%

- India - 46%

- China - 45%

Bloomberg terminal data - 2024 figures

Partly as a result of this risk, Japan has built some buffers -- more than 200 days of commercial and public oil reserves, according to Bloomberg. South Korea, highly dependent on Middle East oil, also has decent buffers: Roughly 200 days. Other Asian nations with reasonably large reserves in storage include Thailand (~100 days), China (~75 days), and India (~65 days). The Philippines, Indonesia, Cambodia, and Vietnam have less than 50 days of reserves.

For much of Asia, these buffers buy time but not immunity. A prolonged disruption in the Strait of Hormuz would quickly translate into fuel shortages, price spikes, and a cascading economic shock across the region.

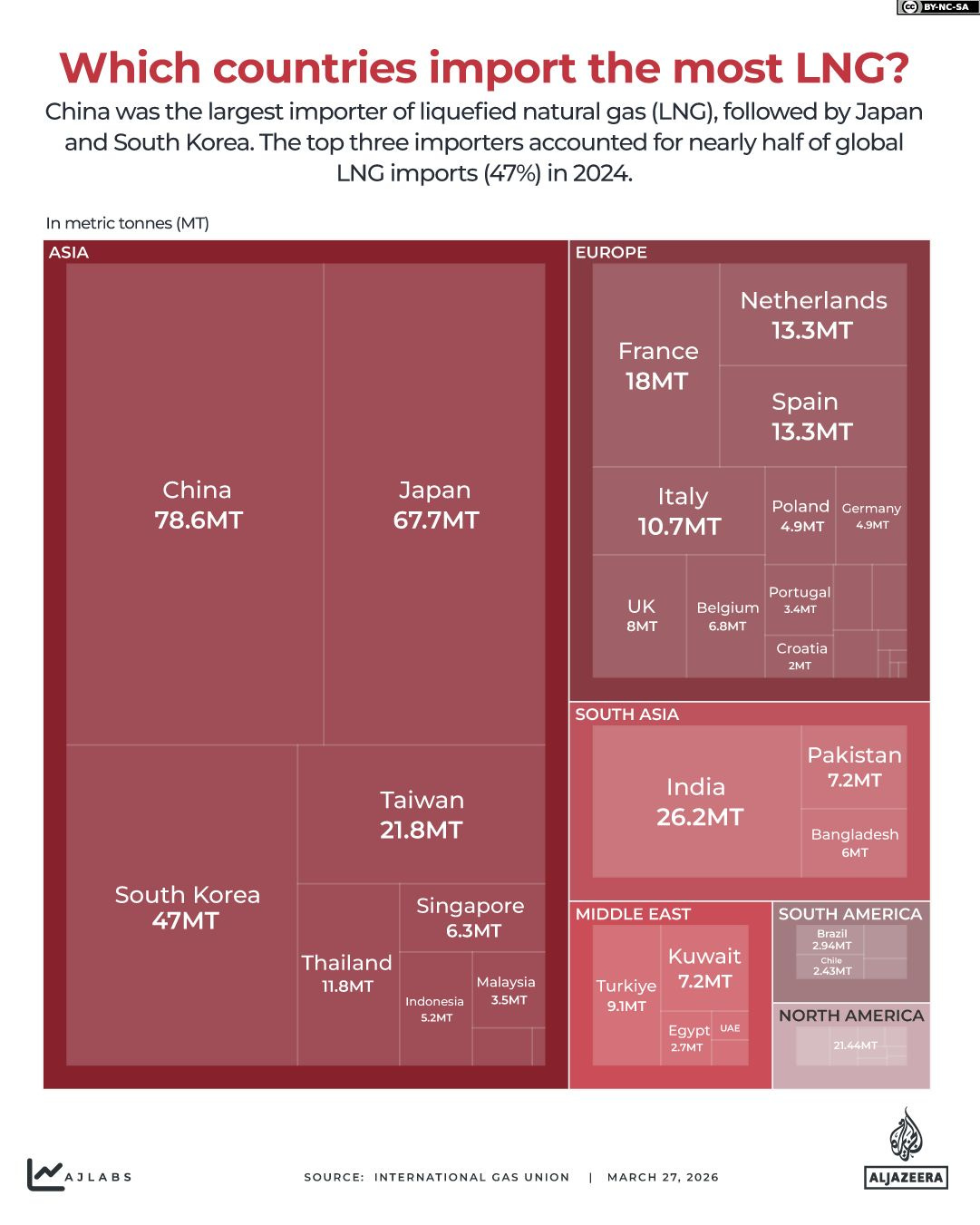

Liquid Natural Gas (LNG) -- Asia’s Industrial Blood

Liquid natural gas has emerged as the bloodstream of the Asian industrial economy. According to Bloomberg data, Qatar is the top LNG provider of 4 of Asia’s top 7 LNG importers. Qatar is the world’s second largest exporter of LNG, eclipsed only by the United States.

Strikes by Iranian missiles and drones on Qatar’s Ras Laffan Industrial City -- the heart of its LNG export infrastructure -- have knocked significant volumes of Qatari gas offline. The damage to liquefaction and processing facilities is expected to take years to fully repair.

“All of Qatar’s LNG production might be offline until the war is resolved,” Bloomberg Intelligence noted, “and at least 17% of the capacity that was damaged by Iranian missiles faces an extended outage.”

Below are the top four LNG global exporters and their percentage share

- The United States - 26%

- Qatar - 19%

- Australia - 18%

- Russia - 7%

- Malaysia - 6%

Source: Bloomberg data

Below are the top LNG importing countries and their percentage share

- China - 15%

- Japan - 15%

- South Korea - 11%

- India - 6%

- Taiwan - 5%

Source: Bloomberg data

And a nifty chart below from Al Jazeera

Qatar was planning a major natural gas capacity expansion, raising their output by 80%, but those plans have been delayed.

And finally…

The following countries are most dependent on LNG imports from Qatar

- Bangladesh - 61%

- India - 46%

- Taiwan - 34%

- China - 29%

- Thailand - 21%

% of LNG imports from Qatar

Source: Bloomberg data

The Hormuz disruption also reshapes the map of opportunity: exporters in the United States, Australia, Malaysia and even Russia stand to capture market share. US LNG, in particular, is well-positioned to fill the gap even if the Strait of Hormuz re-opens as more countries will seek to diversify their energy supply.

Aluminum -- “the biggest supply shock in the history of the market”

Aluminum is a foundational metal for modern industry, embedded in everything from aircraft and automobiles to construction, packaging, and power systems. It’s the most widely used metal after steel.

Before the war, significant volumes of primary aluminum from Gulf Arab producers flowed through the Strait of Hormuz to global markets. Led by major exporters such as the United Arab Emirates, Bahrain, and Qatar, the region accounts for roughly 5–7% of global production but a much larger share -- around 15–20% -- of globally traded primary aluminum, supplying manufacturers across Asia, Europe, and North America.

“The hit to aluminum production in the Middle East threatens to be one of the biggest supply shocks in the history of the market,” Bloomberg Intelligence wrote.

Aluminum production is highly energy-intensive and geographically concentrated, making rapid substitution difficult in the event of sustained disruption. The countries most exposed to Gulf aluminum supply include Japan, South Korea and India. Italy and the United States are also modest importers of aluminum from the GCC states, notably the UAE and Bahrain.

Liquefied Petroleum Gas (LPG) -- The Petrochemical Engine

Often overlooked next to oil and LNG, LPG is a critical household fuel and a key petrochemical feedstock. Before the war, a significant share of globally traded LPG flowed through the Strait of Hormuz to Asia, the primary destination. Saudi Arabia, Qatar, the UAE, and Kuwait anchor global supply, alongside the United States.

Fertilizers -- The Energy-Food Nexus

Fertilizers sit at the intersection of energy and food, with nitrogen-based products like urea and ammonia derived from natural gas. Before the war, substantial volumes flowed from Gulf producers through the Strait of Hormuz to agricultural markets across Asia and Africa. Disruptions are now tightening supply, raising input costs, and exposing import-dependent countries such as India, Pakistan, Bangladesh, and Indonesia to higher food price risks.

Petrochemicals -- Building Blocks of the Modern Economy

Petrochemicals underpin modern manufacturing, embedded in plastics, textiles, electronics, and automotive supply chains. Before the war, significant volumes from Gulf producers moved through the Strait of Hormuz to global manufacturing hubs, particularly in Asia. Saudi Arabia, Qatar, and the UAE are key exporters, with China, India, Indonesia, and Vietnam among the most exposed markets.

Helium -- The Invisible Tech Enabler

Helium is a critical input for semiconductors, fiber optics, medical imaging, and aerospace systems. Before the war, a large share of global supply was provided by Qatar, which accounts for roughly a quarter to a third. Disruptions would ripple quickly through high-tech industries, with China, Japan, and South Korea among the most exposed importers.

Diesel -- The Workhorse Fuel of the Global Economy

Diesel powers freight, agriculture, and industry, making it essential to global trade and food systems. Before the war, large volumes of refined products flowed from Gulf exporters, especially Saudi Arabia, the UAE, and Kuwait, onward through the Strait of Hormuz to Asia, Africa, and Europe. Countries such as India, Pakistan, and Bangladesh are particularly exposed to disruptions in Gulf diesel supply.

Jet Fuel -- The Lifeblood of Global Aviation

Jet fuel underpins passenger travel, air cargo, and the logistics networks that connect modern economies. Before the war, Gulf refiners supplied substantial volumes through the Strait of Hormuz to major aviation hubs across Asia, Europe, and Africa, helping power Asia’s rapid air travel growth. Key exposed markets include India, Singapore, and Thailand, where aviation systems rely heavily on imported fuel.

The Strait of Asia?

In many ways, the Strait of Hormuz is not just a Middle Eastern chokepoint. It also might be dubbed “the Strait of Asia” given its importance to Asia’s growth story. From the factories of China and India to the power grids of Japan and South Korea, Asia’s economic future remains inextricably tied to the free flow of oil and gas and other industrial inputs through this corridor, making its security not a regional concern but a defining pillar of Asia’s continued rise.

That Japanese foreign ministry probably takes little solace in the fact that now the whole world -- and especially Asia -- sees why he spent many a sleepless night thinking about Hormuz.

Afshin Molavi is a geopolitical risk analyst and an emerging markets chronicler. This article was published on Substack. Republished with special arrangement.

What's Your Reaction?

Afshin Molavi

Geopolitical risk analyst. Emerging markets chronicler. Former Reuters, World Bank, Oxford Analytica, emerge85. Recovering journalist. Johns Hopkins SAIS fellow