The $30 Billion Nobody Had to Ask For

Bangladesh’s workers abroad now send home three and a half times what all the world’s donors disburse with no conditions, no consultants, and no debt to repay. It is time to say plainly which model is working.

Deep into a Riyadh night, a Bangladeshi labourer, let us call him Faruk, one of the two and a half million working across the Kingdom, concludes his shift. He returns to his dormitory, taps a mobile application, and transmits 1,500 riyals to Mymensingh. Before his slumber begins, the capital has reached his wife’s digital wallet; by daybreak, it has already been deployed for tuition, medical care, and the corrugated iron that will shield his family from the coming rains.

This transaction required no strategy paper, no visiting mission from a multi-lateral bank, and no bureaucratic oversight. Without the friction of procurement cycles or consultant fees, capital migrated directly from the hands that produced it to the family that required it, allocated with a speed and precision no institutional mechanism can replicate.

Contrast this with the institutional alternative. An assistance loan originates as a strategy document, navigating through assessment teams, complex policy frameworks, and board approvals in distant capitals before reaching Dhaka. It must survive the friction of implementation units, bidding wars, and conditional tranches. Years may pass before it translates into infrastructure or reform -- and while some results are commendable, many projects leave behind only partial progress and a persistent debt obligation.

While both systems facilitate the migration of external capital into a developing economy, a single mechanism has evolved into the primary driver of Bangladesh's trajectory. This engine of growth operates without the fanfare of institutional summits or the oversight of multi-lateral boards.

The Arithmetic of Disproportion

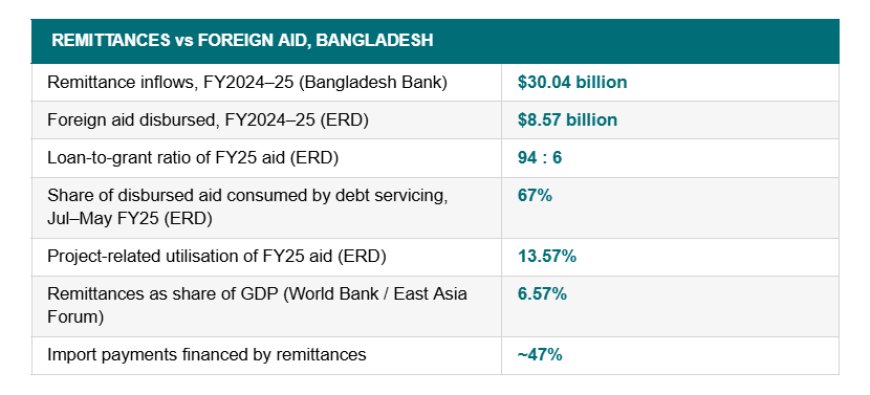

By the conclusion of FY2025, the diaspora had transmitted an unprecedented $30 billion via institutional corridors -- a 25 per cent surge that reflects, in part, the migration of capital from Hundi networks to formal banking following the 2024 political shift. Contrast this against the institutional total: During that same interval, the collective disbursement from every multi-lateral partner -- the World Bank, the ADB, and the UN system included -- amounted to just $8.6 billion.

The three-and-a-half-to-one disparity actually masks a deeper institutional imbalance. The fiscal reality of that FY2025 assistance is stark: A loan-to-grant ratio of 94 to 6 means the term "aid" is largely a misnomer for what is essentially sovereign debt. The friction of the model is further revealed by the fact that 67 percent of disbursements during the July-May interval were immediately consumed by debt servicing on previous obligations. Once we account for interest and principal, the volume of genuinely new capital shrinks to roughly $4.5 billion.

Diaspora transfers, by contrast, possess no amortisation schedules or structural benchmarks; the recipient in Mymensingh incurs no liability to the sender. The institutional failure deepens upon examining the capital's deployment. Official reports from the Economic Relations Division reveal a striking inefficiency: While $8.6 billion entered the treasury in FY2025, a mere 13.57 percent was actually utilized for projects.

This occurred as the Annual Development Program's execution plummeted to a record low of 67.85 percent, suggesting a state apparatus unable to absorb its own debt. Conversely, families face no such administrative paralysis. A diaspora transfer is deployed with near-total efficiency, reaching its terminal objective within forty-eight hours.

Aid is capital that must pass through the state to reach the people. Remittances are capital that reaches the people and then builds the state’s economy from below.

Efficiency at the Kitchen Table

The logic of the diaspora engine is rooted in a fundamental economic truth: The most sophisticated capital allocator for a village home is the family itself. Data from national surveys reveal that these funds flow with fluid intelligence into nutritional security, education, clinical care, and the retirement of predatory debt. Unlike institutional projects with fixed mandates, this capital adapts its priorities in real time as household needs fluctuate. No multi-lateral strategy can match this granular precision, for no board in a distant capital can perceive the intimate realities that a family understands about its own survival.

The resilience of the diaspora engine is best revealed during moments of systemic duress. Institutional finance remains a captive of political cycles, surging when diplomatic interests align and retreating when governance friction or donor fatigue takes hold. Conversely, household capital is profoundly countercyclical and intimate. It accelerated throughout the global pandemic, remained steadfast during the 2022 liquidity crisis, and spiked amidst the 2024 political transition -- operating with a conviction that institutional partners could not muster.

When disaster strikes a coastal village in Barisal, the most agile financial mechanism in existence is a sibling in Dubai equipped with a smartphone. That capital is deployed and utilized before an evaluation team in a distant capital has even finalised its itinerary.

There is a subtler effect that development economists undervalue because it is hard to instrument: Remittances change who rural families must ask. A household with a son in Riyadh does not need the local moneylender at 30 percent, does not need the patronage of the union parishad chairman, does not need to wait for a safety-net card that may require a political favour.

Diaspora income is a private safety net that bypasses every local gatekeeper. That is not merely income. That is a redistribution of power, funded privately, at zero cost to the treasury. The capital itself is profoundly earned -- a reality often relegated to the realm of sentiment, yet one that remains strictly economic. This income is deployed with a rigorous discipline that unearned windfalls can never command.

Academic research into direct transfers continuously rediscovers a truth long understood by the household: Capital governed by the recipient, arriving with the rhythm of predictable obligation and private dignity, is allocated with meticulous precision. A laborer who has endured twelve-hour shifts in the forty-five-degree heat of a construction site does not permit his transmission to be dissipated on the frivolous or the fleeting.

What Aid Actually Is

The institutional alternative follows a divergent logic, requiring a precision that moves beyond mere polemic. This capital is negotiated at the level of states and multilateral boards, entirely bypassing the kitchen table. It arrives encumbered by complex conditionalities; for instance, the prevailing IMF framework demands rigid structural benchmarks for fiscal governance and banking reform.

Its objectives are frequently determined in distant capitals, fluctuating as the priorities of Brussels or Washington pivot toward climate resilience or educational stipends. Before a single cent reaches its terminal objective, it must survive a long institutional journey through ministries, implementation units, and layers of consulting firms -- each extracting a fee and introducing new friction.

Development economists are less diplomatic than the practitioners: A vast corpus of research suggests aid effectiveness is conditional at best, often providing the very fuel for rent-seeking in fragile governance environments. To label the institutional model as futile would be a misstep; it is rather profoundly encumbered.

Each unit of currency must go through extensive administrative steps before it becomes a tangible benefit, and the resulting attrition -- chronic delays, extractive overheads, and systemic capture -- represents the inherent friction of the logic. The gravity of this inefficiency was starkly illustrated in FY2025, when a disbursement of $8.6 billion yielded a project utilization rate of a mere 13.57 percent.

The Honest Counterargument

An honest appraisal demands acknowledging the structural victories of the institutional model, for it has secured outcomes that the diaspora engine, by its very nature, cannot reach. The network of donor-backed cyclone shelters and early-warning protocols transformed a landscape of mass mortality -- from the hundreds of thousands lost in 1970 to the double-digit figures of the present -- representing perhaps the most profound triumph in global disaster mitigation.

It was institutional capital that underwrote the mass immunisation and oral rehydration initiatives that fundamentally broke the back of child mortality. Multi-lateral finance erected the Jamuna Bridge, sustained the primary education stipends that redefined a generation of women, and remains the singular lifeline for a million Rohingya refugees in Cox’s Bazar -- a logistical weight far beyond the capacity of private transfers. Household capital possesses no mechanism to assemble a deep-sea port, an energy grid, or a national embankment system. Challenges of such collective magnitude necessitate institutional coordination, and that coordination remains the domain of sovereign finance.

The costs of remittances are real, and ignoring them only weakens the case. The money is earned at a brutal personal price: Years of family separation; migration debts incurred at 20 to 30 percent interest to pay recruitment agents charging multiples of the legal cap, and exposure to labour regimes with thin protections. A meaningful share of remittance income services the debt taken to earn it.

Some of it funds consumption and status expenditure rather than productive investment. And a remittance economy can become a dependency: Exporting your most energetic young men is not a development strategy so much as a coping strategy that has been running long enough to look like one.

So the question is not whether aid or remittances should exist. Both will. The question is which logic should organise Bangladesh’s development thinking -- and on the evidence, Dhaka has it backwards.

Who Controls the Capital?

When the institutional veneer is removed, these divergent paradigms collide upon a singular axis: The locus of agency. Institutional assistance represents development via the canopy -- capital filtered through multi-lateral boards and bureaucratic layers, eventually reaching the household as the final link in an exhaustive chain.

Conversely, diaspora transfers exemplify development from the roots -- income deployed by the family unit, guided by its own granular intelligence, entirely bypassing the chain. The last thirty years in Bangladesh have served as a lived experiment in these competing logics.

The institutional model, encumbered by consultancy and friction, struggled to utilize a net $5 billion annually. Meanwhile, the engine with no administrative overhead transmitted $30 billion with near-total efficiency, fortifying the national currency, and underwriting half the import bill. It has emerged as a private safety net of such scale that it dwarfs the state’s own social protections in both reach and administrative agility.

The insight here is not the obsolescence of institutions, but rather a truth of economic velocity: External capital achieves its maximum impact when it empowers the household rather than attempting to replace it.

For half a century, the state apparatus has been meticulously engineered to court donor finance -- complete with specialized divisions for negotiation and implementation units for absorption. Yet, no comparable architecture exists to steward diaspora capital, even though it is three-and-a-half times larger in volume. This fundamental imbalance remains the most striking anachronism within the landscape of the country’s economic governance.

What Follows If This Is Right

Treat migrants as development investors, not as labour exports. Lower the cost of sending money -- the gap between the cheapest formal channel and the average one still hands hundreds of millions a year to intermediaries. Beat hundi with a better product, not better policing: faster, zero-fee, mobile-first formal channels with the 2.5 percent incentive delivered in real time rather than through a weeks-long bank reimbursement. Build diaspora savings bonds and investment vehicles that are transparent, liquid, and purchasable on a phone -- India has run this architecture for decades; Bangladesh’s Wage Earner Development Bond remains a product almost no worker has heard of.

Negotiate harder for migrant protection in Gulf labour markets, because wages are the upstream variable that determines everything downstream. And use aid where aid has a comparative advantage -- infrastructure, climate adaptation, skills, safer migration systems -- as the complement to diaspora capital, not the senior partner.

Back in Riyadh, Faruk’s next shift starts at seven. He will send money again at the end of the month, as he has every month for six years, as roughly 13 million Bangladeshis abroad do. No board approves it. No mission evaluates it. It simply arrives, and a school fee gets paid, and a roof gets built, and a small shop stays stocked -- in a hundred thousand villages, every month, without a single conference.

Bangladesh is not primarily being developed from Washington, Tokyo, or even Dhaka. It is being developed from Riyadh, Dubai, Doha, Kuala Lumpur, Rome, London, and New York -- one transfer at a time, by people who never once called it development.

Sudarshan Suvashish Das is General Manager of Regional Markets (Asia, Africa and Middle East) at Ding, a global digital marketplace platform.

What's Your Reaction?