The Long Shadow of Hasinomics

Not only is the government expected to manage the current account deficit, but it is also expected to service the debt obligations it has inherited and pay for its electoral commitments, and yet somehow manage to bring inflation down.

The IMF-World Bank Spring Meetings used to coincide with the cherry blossom week when, well, the flowers blossomed across streets of Washington DC. Climate change means flowers don’t bloom as routinely anymore.

Just as well, because, considering the state of the economy, the Finance Minister and his entourage probably weren’t in any mood to enjoy the flowers when they attended the Spring Meetings last week.

The minister knew he was inheriting an economy stuck in a rut from the Interim Government.

Now he, and we, have a sense of just how weak the economy had been in 2025. The economy grew by 3.6% in the calendar year 2025. Over the year to December quarter, real GDP growth was barely 3% (Chart 1), with a sharp slowdown in the industry sector.

Chart 1: Real GDP Growth (% through the year)

Source: Bangladesh Bureau of Statistics.

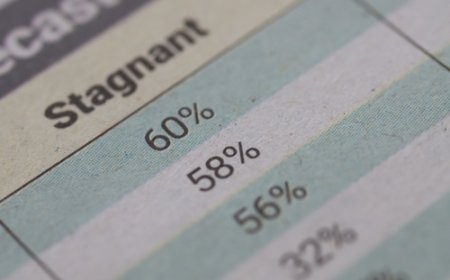

Further, several partial indicators suggest that the weakness has continued into 2026. Industrial production is far weaker than their pre-covid trend, for example, while export growth appears to have peaked (Chart 2). Meanwhile, import growth has also peaked, credit growth continues to slow, and tax revenue has been stagnating (Chart 3).

And all that before the effect of the Iran War had been visible in the data.

Chart 2: Growth in industrial production

and exports (% through the year)

Chart 3: Growth in imports, tax revenue and private sector credit (% through the year)

Source: BBS, Bangladesh Bank, 12-month moving average.

Meanwhile, inflation continues to outpace wage growth (Chart 4), implying an erosion of real income.

The government’s reluctance to remove fuel subsidies, and adjust prices, in the wake of the Iran War has been criticized by economists quite rightly on sound economic grounds. But the political economy of declining real wages probably explain the government’s actions, or lack thereof (though not the miscommunication, but that’s for another time).

Chart 4: Nominal wage growth and Inflation

Nominal wage growth

(% through the year)

Inflation (% through the year)

Source: BBS.

Then came the American-Israeli war on Iran, and the attendant global economic shock. Unsurprisingly, all three major international financial institutions that forecast Bangladesh economy in detail expect stagflation -- sub-par economic growth, and elevated inflation -- in 2026 and 2027 (Chart 5).

Chart 5: Near-term forecasts

Real GDP growth (%)

Inflation (%)

Source: IMF, World Bank, Asian Development Bank. IMF calendar years, others are in fiscal years.

More importantly, the IMF forecasts imply that years of adverse shocks -- the pandemic, energy shocks from Ukraine war and Iran War, macroeconomic mismanagement of the Hasina regime, the Long July, and the prolonged interim administration -- have scarred the economy so much that only a slow and gruelling recovery is likely. Particularly, they don’t expect private investment to recover until later in the decade. Consequently, economic growth recovers to barely a 6% pace, and even that is in 2031. Chart 6 shows this.

Chart 6: Medium-term real economy forecasts

Private investment growth (%)

Real GDP growth (%)

Source: IMF. Private investment growth in fiscal years. Real GDP growth in calendar years.

There is, however far more nuance to the IMF’s medium-term economic projections than one that suggests the entire term of the Tarique Rahman government will be one of economic weakness. Rather, the projections are for not just an eventual investment recovery, but also one of a recovery in household balance sheets.

The economic shocks since the beginning of this decade have seen households dip into their savings, and this is expected to reverse over time. That is a good thing.

Interestingly, the IMF projections also imply that investment will run ahead of domestic savings, and the country will be running a current account deficit to the tune of 2% of GDP by 2031. Chart 7 shows these.

Chart 7: Medium-term Saving-Investment and Current Account forecasts

Savings and Investment (% of GDP)

Current account (% of GDP)

Source: IMF. Calendar years.

Economic theory tells us that a developing country such as Bangladesh should be a capital importer. Experiences in the economies to our north and east is that foreign direct investment has helped spur economic growth. The government wants to attract FDI, and that may well mean running a current account deficit. Plenty of countries have run a deficit of 2% of GDP or larger without facing any difficulties. Sadly, our recent history has not been so successful. Bangladesh was running a CAD of 1% of GDP when the Ukraine War hit the economy, which the Hasina regime failed to manage. The taka depreciated by around 40%, despite the central bank losing nearly half of the stock of reserve.

However, when one parses the IMF figures, something interesting emerges. They don’t report it directly, but it turns out that their forecasts reflect an exchange rate trajectory to only around 140 taka per US dollar by the end of the decade. That is, the expectation here is that the government will manage the banking and financial sectors well enough so that the current account deficit will not lead to a run on the taka!

In fact, there is more. The forecasts are for between a quarter and a third of revenue to go toward interest expenditures -- the long shadow of the Hasinomics will be with us for a long time to come.

However, not only is the government expected to manage the current account deficit, but it is also expected to service the debt obligations it has inherited and pay for its electoral commitments, and yet somehow manage to bring inflation down.

And yes, you did read that right. The IMF expects inflation to subside sharply next year. Chart 8 shows this.

Charts 8: Medium-term Interest Payments and Inflation forecasts

Interest expenditure (% of revenue)

Inflation (%)

Source: IMF. Calendar years.

The Finance Minister clearly didn’t have a successful meeting with the IMF. But their forecasts suggest that the institution has a degree of confidence in his ability to manage the macroeconomy.

However, these forecasts also make it clear that there is no immediate economic lift-off in sight, and tough times await.

At the very least, the government needs to do a better job of explaining to the people that the economy is facing a complex conjuncture.

Jyoti Rahman is the Executive Editor of the weekly Counterpoint.

What's Your Reaction?